GLOSSARY OF TERMS

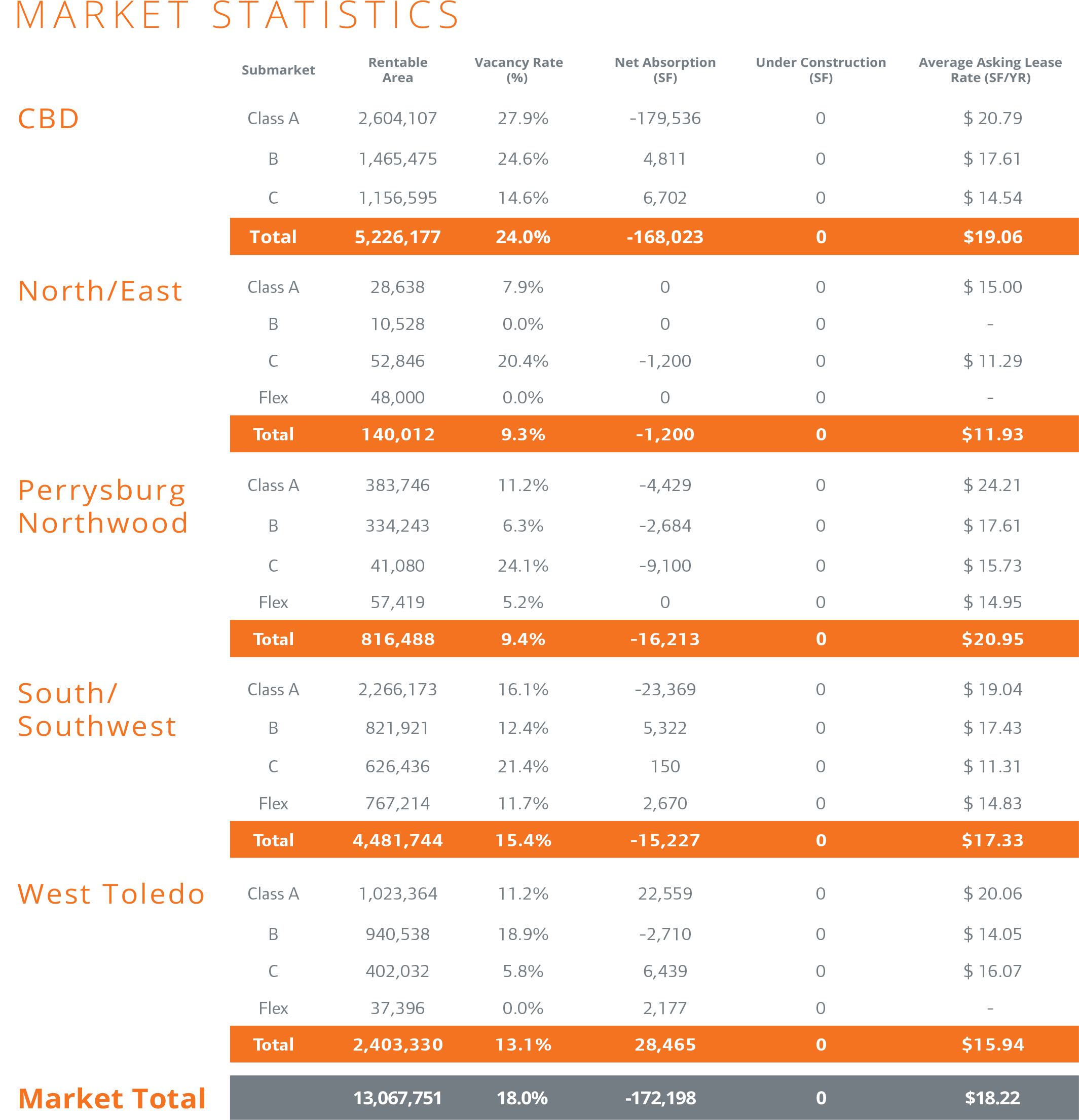

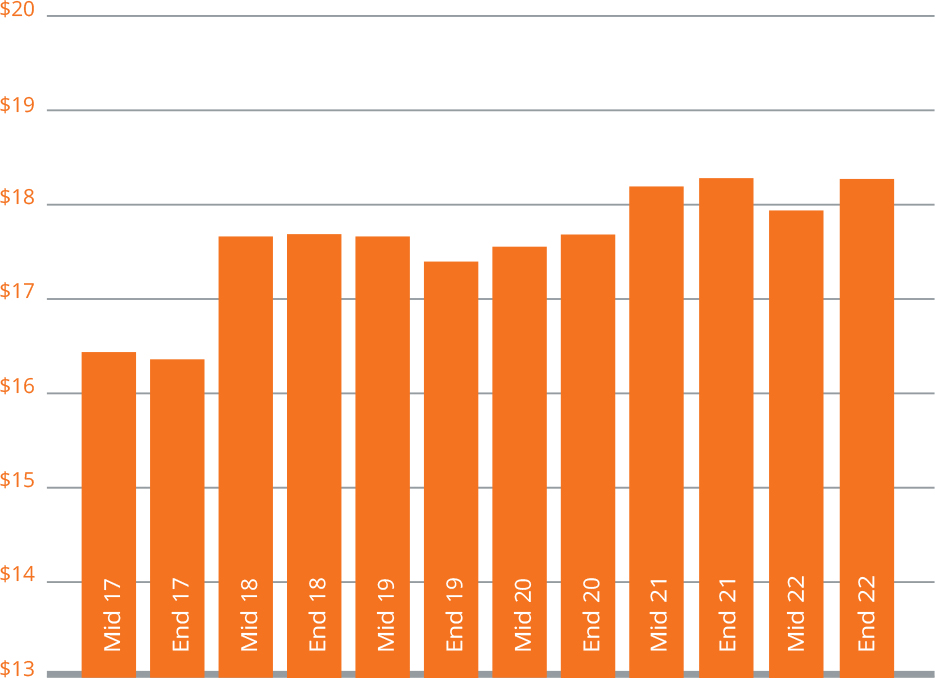

Average Asking Lease Rate: Rate determined by multiplying the asking net lease rate for each building by its available space, summing the products, then dividing by the sum of the available space with full-service gross leases for all buildings in the summary.

Net Leases: Includes all lease types whereby the tenant pays an agreed rent plus most, or all, of the operating expenses and taxes for the property, including utilities, insurance and/or maintenance expenses.

Market Coverage: Includes all competitive office buildings 5,000 square feet and greater in size.

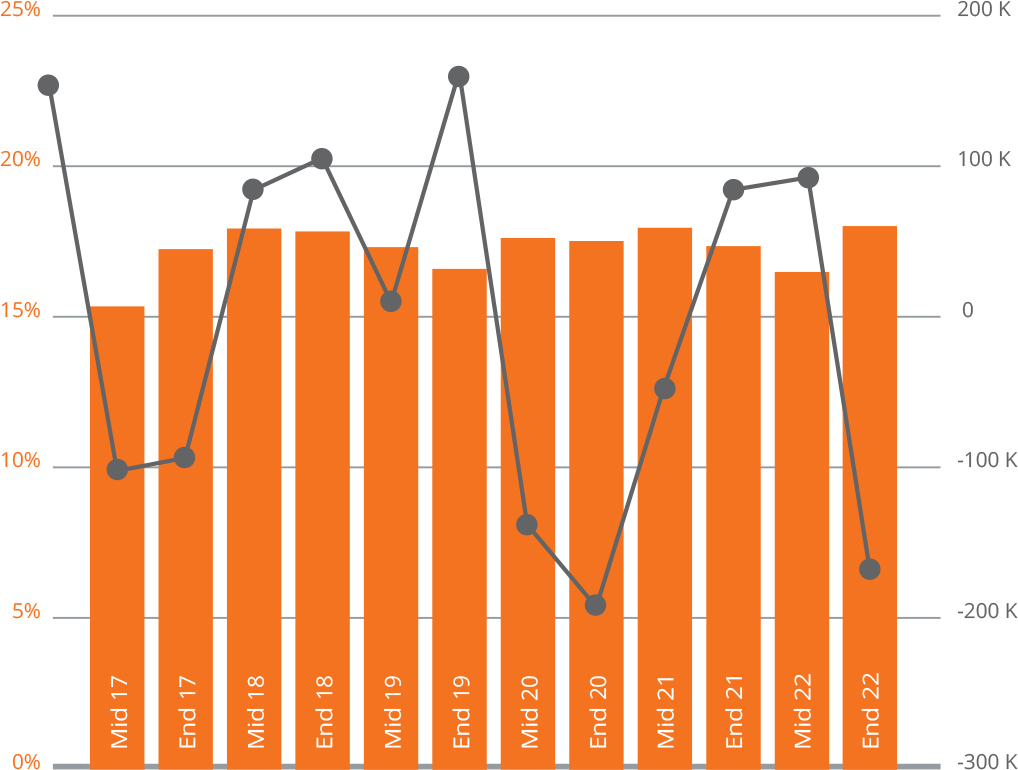

Net Absorption: The change in occupied square feet from one period to the next.

Net Rentable Area: The gross building square footage minus the elevator core, flues, pipe shafts, vertical ducts, balconies and stairwell areas.

Occupied Area (Square Feet): Building area not considered vacant.

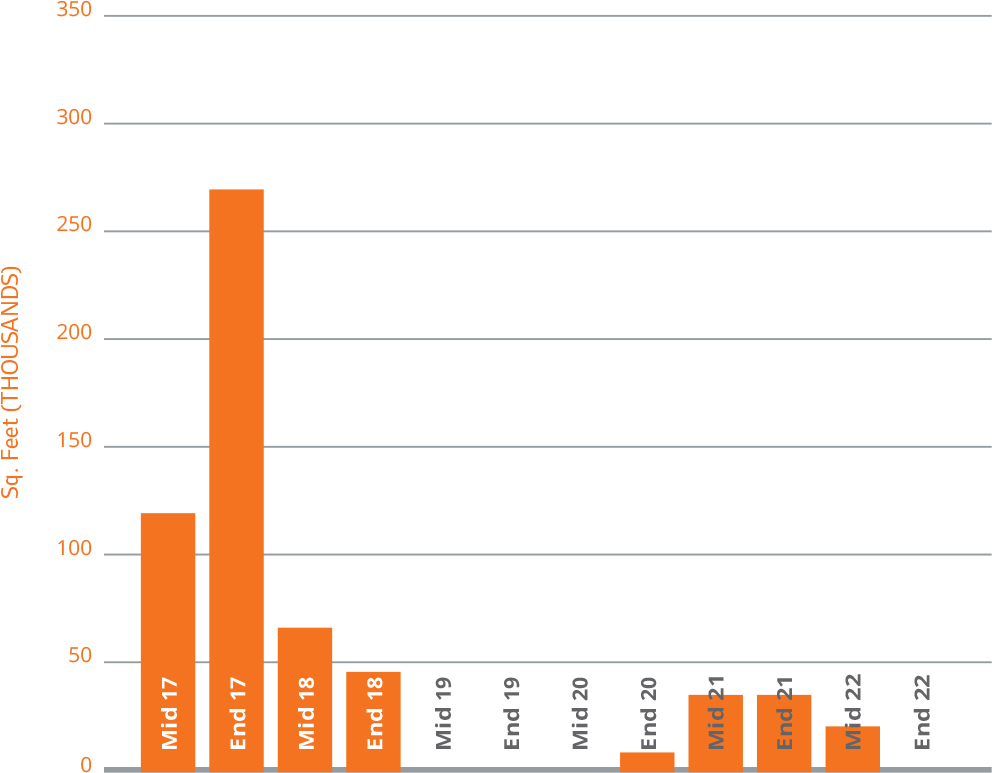

Under Construction: Buildings which have begun construction as evidenced by site excavation or foundation work.

Available Area (Square Feet): Available Building Area which is either physically vacant or occupied.

Availability Rate: Available Square Feet divided by the Net Rentable

Vacant Area (Square Feet): Existing Building Area which is physically vacant or immediately available.

Vacancy Rate: Vacant Building Feet divided by the Net Rentable Area.

Normalization: Due to a reclassification of the market, the base, number, and square footage of buildings of previous quarters have been adjusted to match the current base. Availability and Vacancy figures for those buildings have been adjusted in previous quarters.